Jump to winners | Jump to methodology

Excellence beneath strain: how America’s prime claims insurers are successful dealer belief

Sixteen US insurance coverage carriers have earned Insurance coverage Enterprise America’s 5-Star Claims designation for 2026, as rated by brokers throughout the nation on claims administration, communication, and operational effectivity. This report identifies which corporations earned the designation and what they do otherwise.

Introduction – The strain cooker:

US business claims in 2026

American brokers have a easy take a look at for the carriers they suggest: be there when it issues. In business insurance coverage claims – the second of reality in each coverage – that take a look at is tougher than ever to move in 2026. Rising litigation severity, nuclear verdicts, and a litigation funding {industry} pouring billions into plaintiff-side circumstances have made the US claims setting one of the difficult on the planet. Towards that backdrop, Insurance coverage Enterprise America’s 5-Star Claims 2026 report identifies one of the best insurers for claims within the US, as rated by brokers throughout the nation.

The 2026 designation was awarded following a complete two-phase broker-rated analysis course of. Brokers have been first invited to appoint the insurers they believed delivered one of the best claims administration and claims dealing with, ranking them throughout key efficiency indicators. Carriers that acquired ample dealer nominations have been then invited to submit detailed proof of their claims capabilities. Ultimate designations have been awarded to these organizations that achieved excellent dealer rankings whereas additionally demonstrating excellence in claims administration, operational effectivity, and dealer engagement. Sixteen insurers earned the 5-Star Claims designation for 2026.

The 16 insurers that earned the 5-Star Claims designation for 2026 are the next:

The findings level to a transparent sample – the carriers brokers belief most for business insurance coverage claims are those who:

-

talk with consistency

-

deploy specialist experience

-

use know-how to free their individuals to train judgment, to not substitute it

Trade context – What brokers demand

in 2026

The hole between what brokers anticipate from claims service and what insurers truly ship has a single, constant root trigger: communication. Based on Sean O’Neill, associate and head of the worldwide insurance coverage follow at Bain & Firm in Boston, responsiveness and transparency are the 2 qualities brokers worth most – and the inconsistency of communications stays the most important disconnect within the claims course of.

“The inconsistency of communications is the most important disconnect between the events concerned within the claims course of throughout purchasers, brokers, and carriers”

Sean O’NeillBain & Firm

Brokers don’t simply need info; they need to know what is going on, why it’s occurring, and what occurs subsequent. O’Neill notes that expectations have developed not in precept however in kind and pace – the bar for a way shortly and clearly info have to be delivered continues to rise, formed by the digital experiences professionals have in each different space of their lives.

The information from JD Energy’s analysis confirms this image. Based on the JD Power 2025 US Claims Digital Experience Study, launched December 2, 2025, receiving sufficient digital updates is the highest driver of claims satisfaction – but insurers ship on this key efficiency indicator simply 22 % of the time. Total satisfaction with the auto insurance coverage claims course of stands at 700 on a 1,000-point scale, per the JD Power 2025 US Auto Claims Satisfaction Study (October 28, 2025), based mostly on responses from 9,455 prospects of the biggest US suppliers. Mark Garrett, director of world insurance coverage intelligence at JD Energy, identifies proactive communication as the only most vital issue separating the best-rated claims insurers from the remainder.

“Lots of the insurers who excel in our research have a stability of tech and human contact, with a key differentiator being eliminating the necessity for the shopper to name”

Mark GarrettJD Energy

Garrett’s analysis reveals that cellular app experiences now obtain a satisfaction rating of 775 towards the general research common of 700 – a 75-point hole. Apps carry out significantly nicely on lower-severity claims the place prospects who start the method digitally have a tendency to remain in that channel; nonetheless, solely 36 % of auto insurance coverage prospects presently obtain standing updates through cellular app, regardless of app-based claims dealing with attaining the very best satisfaction scores. The very best-performing carriers are those who layer digital effectivity over – relatively than as a substitute of – human experience.

That experience isn’t a commodity. O’Neill argues that whereas specialist data in claims dealing with is important, it’s essential however inadequate by itself. The true foreign money of a claims relationship is belief – constructed or destroyed at each stage of the claims administration course of, from first discover of loss via closing decision.

How nuclear verdicts are reshaping

US claims

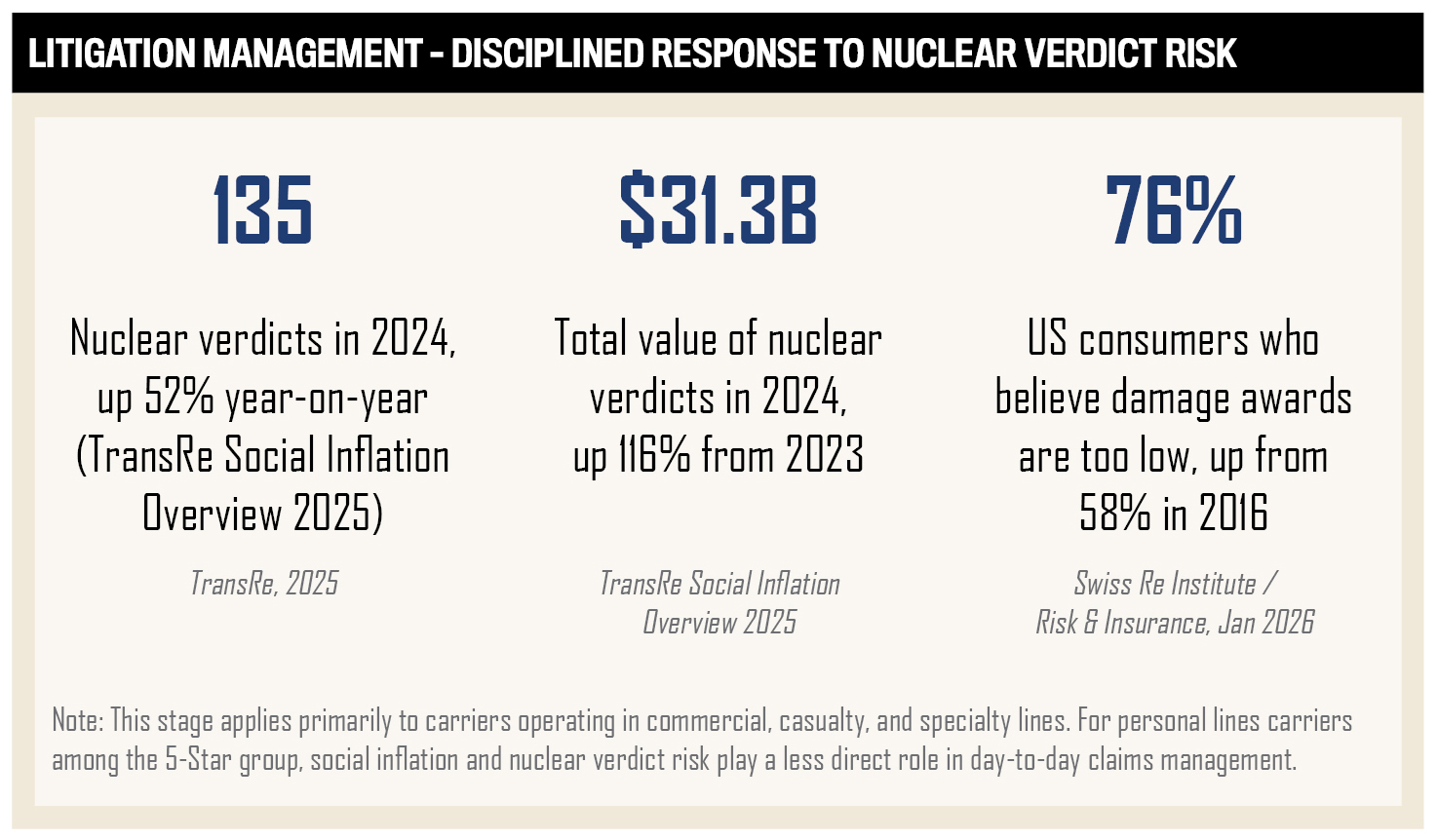

The US litigation setting amplifies the stakes of each claims choice. In 2024, there have been 135 lawsuits leading to nuclear verdicts – jury awards exceeding $10 million – towards company defendants, a 52 % enhance over 2023, in keeping with TransRe’s Social Inflation Overview 2025. The overall worth of these verdicts reached $31.3 billion, representing a 116 % enhance from the prior yr.

The cultural forces driving this development are measurable. Based on Swiss Re Institute analysis revealed by Danger & Insurance coverage in January 2026, 76 % of US customers now consider injury awards are too low – up from 58 % in 2016. That 18-percentage-point shift in public angle over 9 years has basically reshaped what juries think about honest compensation, with direct penalties for business traces claims dealing with throughout the market.

Legal professional promoting and third-party litigation funding have compounded the issue. The US business litigation finance {industry} managed $16.1 billion in belongings throughout 42 lively capital suppliers from mid-2023 to mid-2024, in keeping with the Westfleet Advisors 2024 Litigation Finance Report – offering the plaintiffs’ bar with institutional-scale sources to fund high-value circumstances. For carriers managing business insurance coverage claims, this setting calls for rigorous investigation, specialist protection counsel, and a transparent strategic strategy to litigation administration.

The median verdict in circumstances over $10 million grew from $19.3 million in 2010 to $24.6 million in 2019 – a 27.5 % enhance that outpaced the overall inflation fee of 17.2 % over the identical interval, per a research of 1,376 such verdicts cited by the US Chamber of Commerce Institute for Authorized Reform. The very best-rated claims insurers within the 2026 IBA report have constructed their operations particularly to navigate this setting.

The median verdict in circumstances over $10 million grew from $19.3 million in 2010 to $24.6 million in 2019 – a 27.5 % enhance that outpaced the overall inflation fee of 17.2 % over the identical interval, per a research of 1,376 such verdicts cited by the US Chamber of Commerce Institute for Authorized Reform. The very best-rated claims insurers within the 2026 IBA report have constructed their operations particularly to navigate this setting.

A construction constructed to eradicate delay

When Richard Wolff, managing director of casualty claims at Markel Insurance in New York, describes what makes his casualty claims operation efficient, he doesn’t attain for superlatives about know-how or proprietary methods. He factors to one thing extra basic: the way in which the group is constructed.

Markel’s claims operation is intentionally flat. There are a couple of ranges between a desk adjuster and the chief claims officer, and that construction isn’t incidental – it’s by design. In a claims setting outlined by rising severity and more and more advanced business traces litigation, the flexibility to escalate a choice shortly and attain the suitable reply sooner than rivals is a tangible aggressive benefit.

That flatness additionally shapes the tradition. Senior management at Markel is accessible and approachable – a working setting the place workers really feel supported and engaged, and the place engaged workers interprets instantly into higher claims dealing with outcomes for insureds and dealer companions.

Markel’s 2026 IBA submission reinforces this image. The service has invested in deep product-specific specialization – claims groups organized round particular person traces of enterprise relatively than generalist swimming pools. The philosophy extends to specialist experience at each stage, from a advantageous arts claims specialist with expertise at Sotheby’s to equine and agriculture specialists who’re horse homeowners or former veterinary technicians. The idea is that nuanced data of a shopper’s world drives higher claims administration choices.

Up to now 24 months, Markel has continued a structured modernization of its claims platform, rolling out ClaimCenter to enhance real-time information capabilities, workflow visibility, and loss run reporting. The service has additionally accelerated litigation administration initiatives in direct response to the social inflation and nuclear verdict threat, reshaping the US casualty and business traces claims panorama.

“Extra layers imply delay. So I believe we’re geared up and designed in a technique to eradicate or definitely decrease these delays”

Richard WolffMarkel Insurance coverage

Wolff’s evaluation of the litigation problem is direct. Declare severity in the USA continues to extend, pushed by lawyer promoting, litigation funding, and what he describes as a broader public immunity to massive greenback quantities – the identical dynamic recognized within the Swiss Re Institute and TransRe analysis. Markel’s response is constructed on three pillars: rigorous investigation, glorious protection counsel, and a demonstrated willingness to take circumstances to verdict when applicable. With out that willingness, Wolff argues, a service indicators to the plaintiffs’ bar that it’s going to at all times settle, which in the end means overpaying on all the pieces.

Q&A: Richard Wolff, Markel Company

Q: How is AI presently getting used inside Markel’s claims operation, and what’s your total philosophy on its position?

A: We’re within the toddler levels, however it’s definitely not rising like an toddler – the pace of improvement is fascinating. We now have Copilot embedded in our claims system, and we’re piloting quite a lot of purposes to have AI help with triage. The objective is to create efficiencies that liberate time for extra analytical work. AI adjustments day by day, and whereas it’s designed to help the human course of, it nonetheless requires validation. I inform my group: use no matter instruments can be found to make you extra environment friendly, however on the finish of the day, no matter you utilize AI for, the end result must be appropriate. We nonetheless personal the end result.

Q: How do you consider the stability between AI effectivity and human judgment in claims?

A: I’d analogize it to having 14 golf equipment in your golf bag. Good gamers change them out relying on what course they’re on – however on the finish of the day, it’s the participant and the swing that creates the ball going within the gap. AI is a type of golf equipment. I can use it to assist get to the suitable declare end result. However you can not flip a blind eye and say regardless of the bot says is the product. There have been attorneys who’ve gone sideways by permitting AI to put in writing authorized briefs that cited case legislation that didn’t exist. Judges don’t significantly look after that. Neither would I if my group produced one thing fallacious.

Q: What are essentially the most concrete methods you need to use automation and AI to enhance the worker expertise?

A: We now have a pilot taking a look at automating our triage processes to have a file instantly assigned to an examiner. Liberating up supervisor time provides them the chance to be extra analytical and fewer administrative. It is perhaps onerous to quantify the acquire instantly, however I can inform you anecdotally that it’s going to make my 15 managers extremely blissful – and blissful means engaged. An engaged workers results in higher outcomes. One feeds the opposite.

Q: Markel’s casualty claims group earned the 5-Star Claims designation based mostly on dealer rankings. What does that recognition imply

to you?

A: I’ve the privilege of getting this dialog, however I don’t do the work. The credit score goes to the individuals in my group. They’re those dealing with claims day by day – my examiners and managers. If somebody thought extremely sufficient of us to appoint us and brokers rated us the way in which they did, that displays the consistency and requirements of the individuals doing the day-to-day work. I need to make that clear.

What a 5-Star claims course of appears like

What separates the 16 insurers awarded the 2026 IBA 5-Star Claims designation from the broader market isn’t a single functionality or funding – it’s a course of. Throughout each submission, interview, and dealer ranking on this yr’s analysis, a constant six-stage framework emerges: the carriers that brokers belief most observe the identical basic arc, from first discover of loss to decision, no matter their measurement, construction, or line-of-business combine.

The information from the 2026 winner submissions make this seen in quantifiable phrases. Each submitting winner deploys AI or analytics instruments – 100% adoption among the many 5-Star group. And each single submission – with out exception – names constant, proactive communication as a major differentiator. That final discovering is essentially the most instructive, as a result of JD Energy’s 2025 US Claims Digital Expertise Examine reveals that insurers ship sufficient proactive updates simply 22 % of the time throughout the market. The 5-Star carriers are the exception, not the norm.

The six levels under symbolize what the best-performing claims operations within the US persistently do, drawn instantly from the 2026 winner submissions and dealer analysis. They don’t seem to be aspirational. They’re noticed.

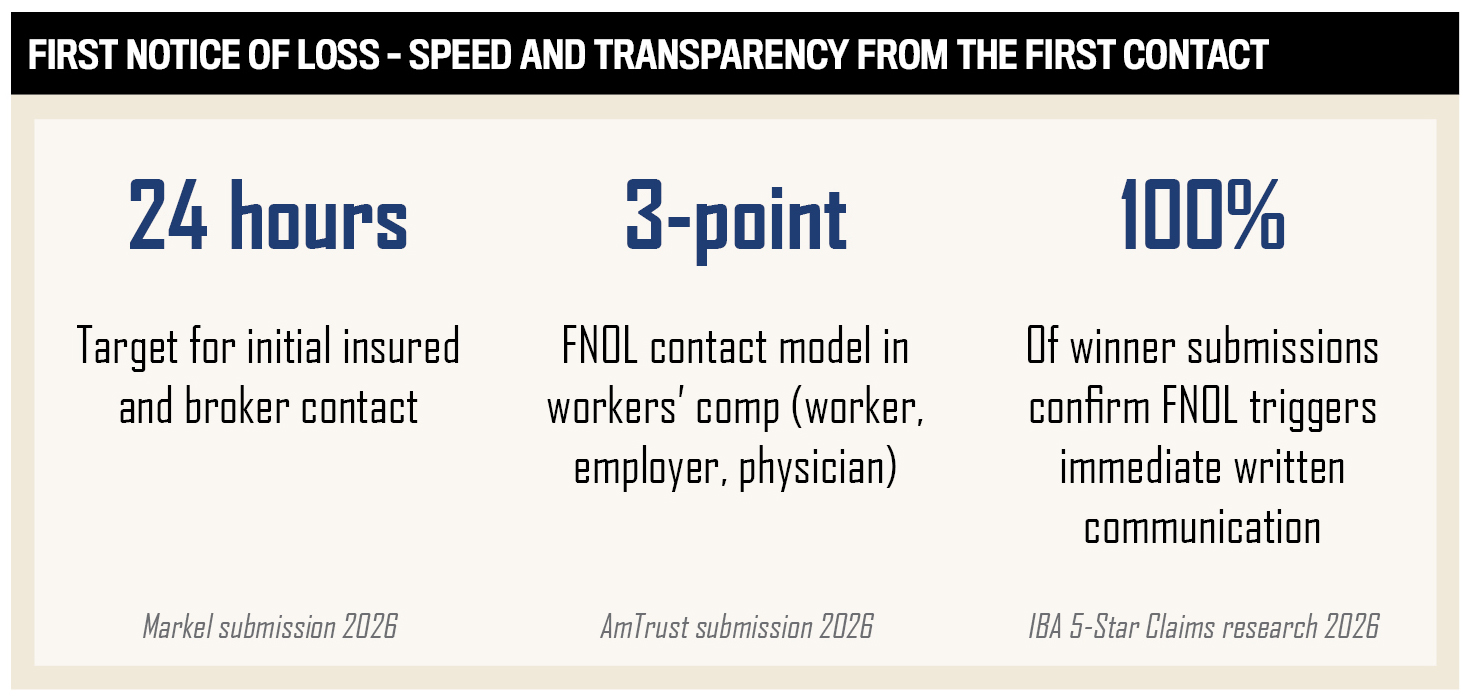

Stage 1: First discover of loss – pace and transparency from the primary contact

The 5-Star course of begins earlier than the claims group has all of the information. Winners acknowledge claims promptly – usually inside 24 hours – and attain out on to each the insured and dealer. An preliminary protection place is established as shortly as potential and confirmed in writing, setting clear expectations from the outset. In employees’ compensation, this extends to simultaneous three-point contact between the injured employee, employer, and treating doctor from the second a declare is filed.

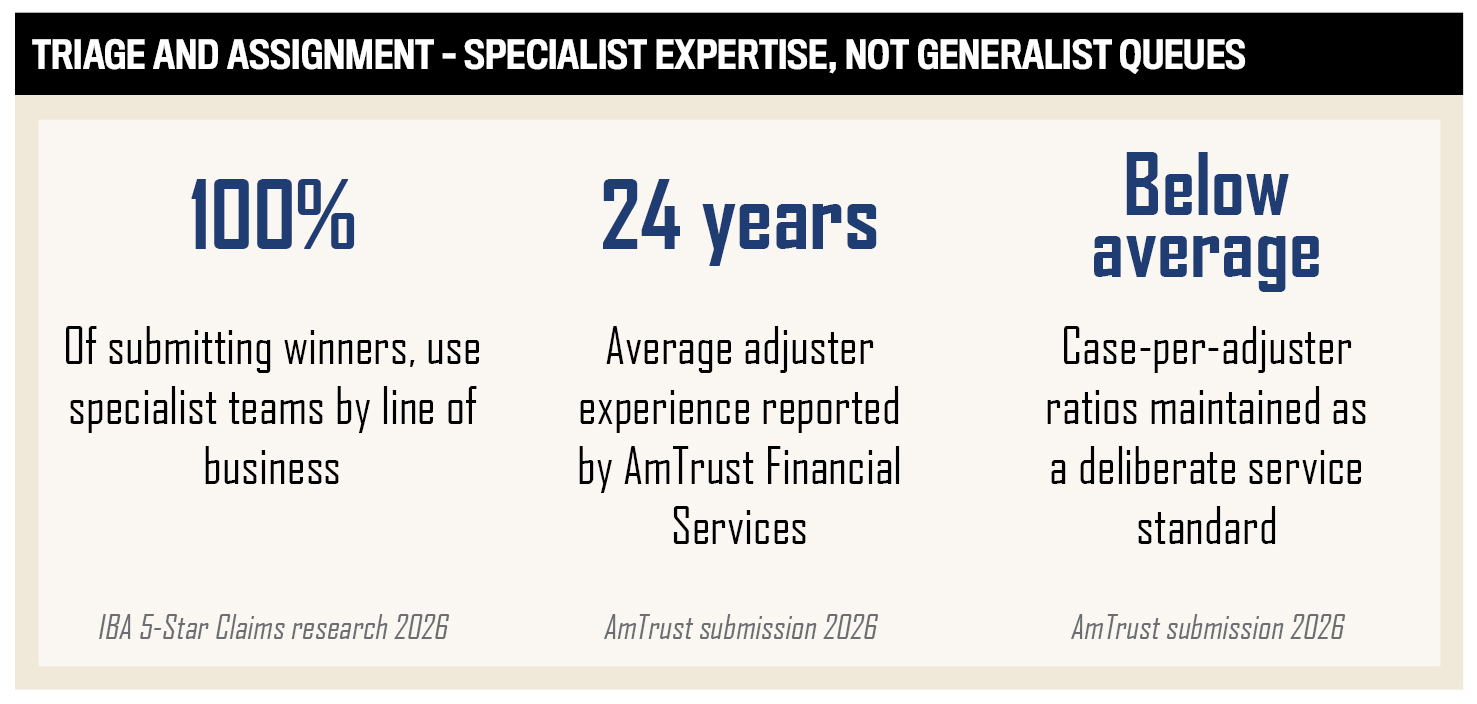

Stage 2: Triage and task – specialist experience, not generalist queues

Each submitting winner routes claims to devoted specialist groups organized by line of enterprise, by no means to generalist swimming pools. Deep product-specific experience is handled as a aggressive necessity: Markel’s advantageous arts claims specialists have labored at Sotheby’s; its equine claims specialists are horse homeowners or former veterinary technicians. AmTrust Monetary Providers experiences that its adjusters common 24 years of {industry} expertise and preserve below-industry case-per-adjuster ratios to make sure targeted consideration on each file. Complicated and extreme losses are escalated to devoted specialist items relatively than dealt with in the usual workflow.

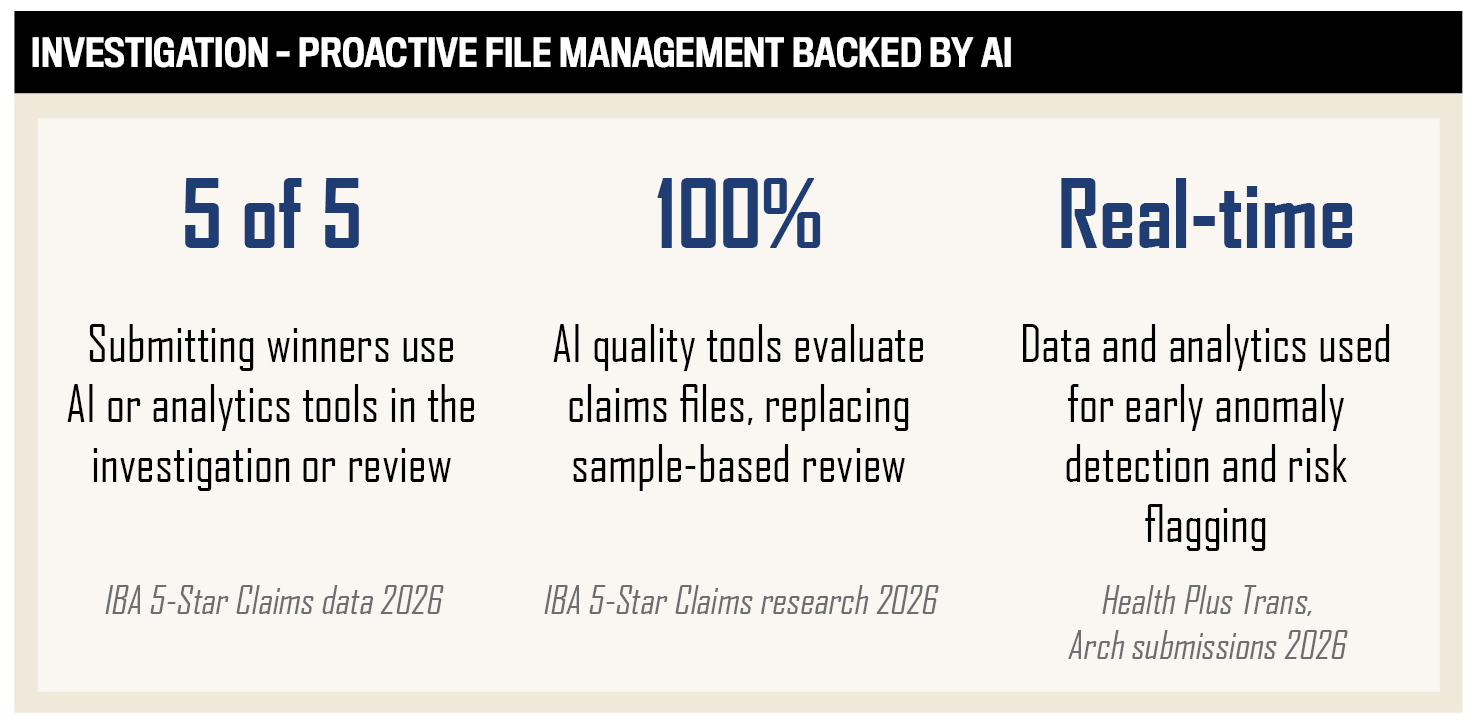

Stage 3: Investigation – proactive file administration backed by AI

Winners handle recordsdata proactively, with continuous reassessment as information evolve relatively than periodic milestone critiques. AI instruments are deployed for file assessment, anomaly detection, fraud flagging, and high quality scoring – however in each case, the human adjuster retains possession of the end result. The very best operations deploy AI high quality instruments that consider claims recordsdata constantly relatively than on a pattern foundation, offering real-time suggestions to adjusters and supervisors and elevating the general customary of file dealing with.

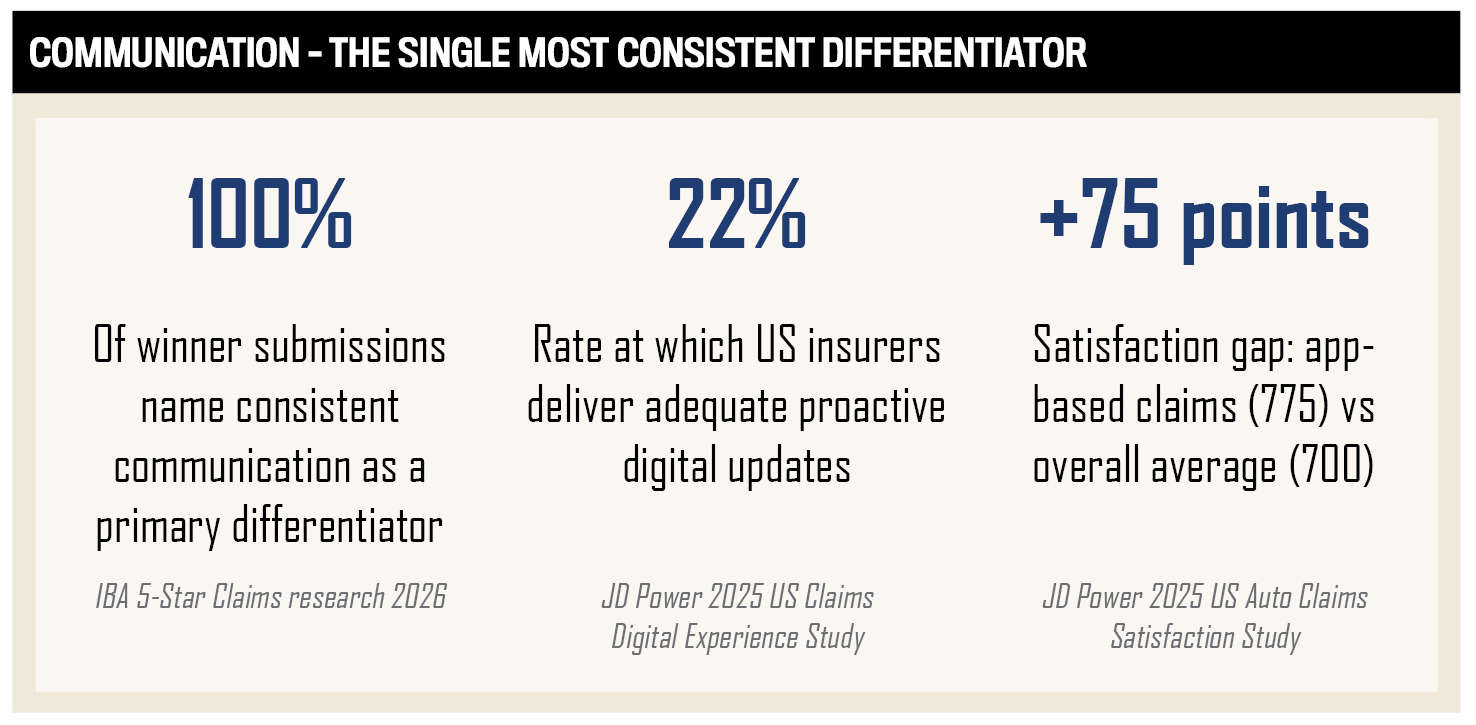

Stage 4: Communication – the only most constant differentiator

Communication is the only discovering that runs via each submission, each interview, and each dealer ranking within the 2026 analysis. All 5 submitting winners describe it as a core pillar of their claims operation, not a downstream operate. The very best performers ship proactive standing updates – not solely when the insured calls – from first discover of loss via closing decision. Settlement methods and protection positions are defined clearly and confirmed in writing. Digital channels, together with safe two-way texting platforms, cellular app updates, and automatic notifications, are used to eradicate the necessity for follow-up calls fully.

“The inconsistency of communications is the most important disconnect between the events concerned within the claims course of throughout purchasers, brokers, and carriers”

Sean O’NeillBain & Firm

JD Energy’s 2025 US Claims Digital Expertise Examine places the stakes in stark reduction: regardless of proactive communication being the primary driver of claims satisfaction, US insurers ship it adequately simply 22 % of the time. The 5-Star carriers have turned that hole right into a structural benefit.

Stage 5: Litigation administration – disciplined response to nuclear verdict threat

In a market formed by nuclear verdicts and social inflation, litigation administration is not a back-office operate – it’s a front-line differentiator. The 5-Star carriers strategy it with strategic intent. Markel’s Richard Wolff describes a three-pillar response: rigorous investigation on each file, the deployment of specialist protection counsel, and a demonstrated willingness to take circumstances to verdict when applicable. That final component is deliberate – with out it, a service indicators to the plaintiffs’ bar that it’s going to at all times settle, which in the end means overpaying on all the pieces.

A number of winner submissions reference accelerated funding in litigation administration prior to now 24 months, with real-time analytics used to determine litigated-claim traits on the portfolio stage and refine protection technique accordingly. In-house protection counsel is engaged early on advanced recordsdata relatively than at escalation. Allocation and different insurance coverage issues are addressed proactively relatively than at dispute.

Stage 6: Decision and closure – pace, selection, and closed-loop studying

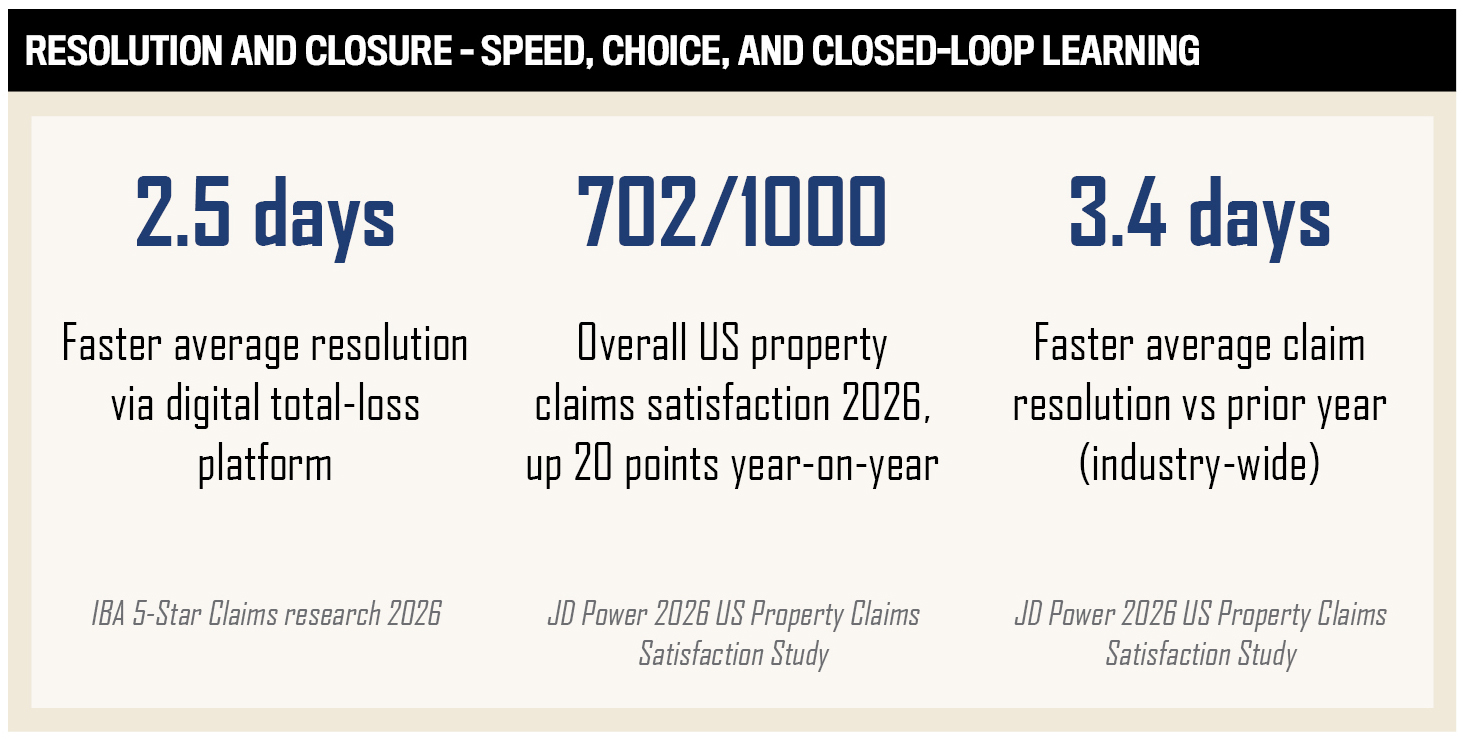

The 5-Star course of doesn’t finish at settlement – it loops again into the group. Winners observe cycle time and file closure as major efficiency metrics, reporting them transparently towards set operational targets. Trendy fee choices, together with PayPal and Venmo, can be found to cut back friction at closing disbursement. For complete loss auto claims, main carriers deploy devoted digital platforms that coordinate the insured, insurer, and third-party distributors in a single workflow, considerably lowering decision time.

Critically, winners feed decision information again into the broader group. Declare insights and traits are shared with underwriting and actuarial companions, in order that closure isn’t the tip of the declare’s worth – it’s the starting of higher threat decision-making. JD Energy’s 2026 US Property Claims Satisfaction Examine confirms that this focus is delivering: total {industry} satisfaction rose 20 factors to 702, with claims resolved 3.4 days sooner than the prior yr.

The human-technology stability: the thread throughout all six levels

Throughout all six levels, one precept holds fixed among the many 2026 5-Star winners: know-how serves individuals, not the opposite approach round. Each submitting winner makes use of AI or analytics instruments – however everybody frames AI as an effectivity layer that frees skilled adjusters to train the judgment, empathy, and relationship-building that know-how can’t replicate. Markel’s Wolff places it plainly: AI is certainly one of 14 golf equipment within the bag. The participant and the swing nonetheless decide the end result.

That stability is tougher to attain than it sounds. Based on a Sedgwick report coated by Danger & Insurance coverage in April 2026, solely 7 % of property insurance coverage carriers have achieved scalable AI success in claims operations – regardless of practically two-thirds acknowledging a spot between their AI ambitions and present actuality. The 5-Star carriers are constructing in each instructions concurrently: modernizing their know-how stack whereas deepening the specialist human experience that offers know-how its context. That mixture, repeated persistently throughout six levels of a claims lifecycle, is what dealer belief is constructed on.

Trade outlook – the subsequent frontier

The query going through one of the best claims operations in the USA isn’t easy methods to match present expectations – it’s what comes after them. The JD Energy 2026 US Property Claims Satisfaction Examine provides an encouraging baseline: total satisfaction rose 20 factors to 702, with claims resolved 3.4 days sooner than the prior yr. That enchancment is actual. However it’s also uneven, and the carriers that outline the subsequent benchmark will likely be those who perceive exactly the place the gaps stay.

Sean O’Neill at Bain is direct about the place funding has and has not landed. Vital focus has been positioned on first discover of loss, consumption, and the related triage – essentially the most seen and digitally tractable elements of the claims lifecycle. Much less consideration has been paid to investigation, settlement, and subrogation. These are tougher to automate, tougher to measure from the skin, and tougher to distinguish on. They’re additionally the place essentially the most consequential claims choices are made, and the place the hole between one of the best carriers and the remainder is widest.

“A whole lot of focus has been put into FNOL and consumption and the related triage, however much less consideration has been targeted on the opposite elements of the method, together with investigation, settlement, and subrogation”

Sean O’NeillBain & Firm

For business traces carriers specifically, closing this hole requires the identical self-discipline in investigation and settlement technique that one of the best operations already apply to litigation administration. The 5-Star carriers have demonstrated that systematic funding throughout the total claims lifecycle – not simply its most seen levels – is what produces constant dealer belief over time.

Loss prevention: from reactive to proactive

Past closing current course of gaps, the extra transformative shift on the horizon is the transfer from reactive claims administration to proactive loss prevention. The indicators from related gadgets, telematics-equipped automobiles, and good constructing methods are creating a real alternative for carriers to assist purchasers scale back and forestall losses earlier than they happen – a basically totally different working mannequin from the one the {industry} has run for a century.

O’Neill at Bain argues that there must be an inflection within the complete value of threat within the {industry}, and that loss prevention will play an outsized position in getting there. The mechanics are easy in precept: a service with entry to real-time IoT information from a business property can determine a failing HVAC system, a sprinkler strain drop, or uncommon after-hours entry earlier than they grow to be a declare. A telematics-equipped fleet can floor high-risk driving habits earlier than it produces a legal responsibility occasion. The identical information infrastructure that powers fashionable claims administration can, in principle, be redeployed upstream.

In follow, this requires a major operational transformation. Most carriers weren’t constructed to ship advisory companies or real-time threat monitoring at scale. The carriers finest positioned to capitalize on loss prevention will likely be those who have already invested within the information infrastructure, analytics functionality, and client-facing communication frameworks that fashionable claims administration calls for – as a result of those self same foundations are exactly what proactive loss prevention requires.

What the subsequent benchmark appears like

The 2026 5-Star Claims winners symbolize the present customary. The subsequent benchmark will belong to carriers that reach that customary into the elements of the claims lifecycle which have acquired the least funding – investigation, settlement, and subrogation – whereas concurrently constructing the potential to shift from responding to losses to stopping them.

For brokers, the implication is evident: the carriers value recommending in 2027 and past won’t simply be those that deal with claims nicely once they arrive. They would be the ones who demonstrably assist purchasers arrive at fewer claims within the first place. That may be a larger bar than any dealer satisfaction survey presently measures – and it’s the place essentially the most forward-thinking carriers within the 2026 5-Star group are already wanting.

The 16 insurers acknowledged within the 2026 IBA 5-Star Claims report didn’t earn dealer belief by chance. Throughout organizations of various sizes, buildings, and line-of-business mixes, a constant image emerges: one of the best claims insurers are flat sufficient to make choices shortly, specialised sufficient to carry real experience to each file, and disciplined sufficient to make use of know-how as a software relatively than a shortcut.

They convey clearly and persistently – from first discover of loss via closing decision. They rent individuals who know their purchasers’ worlds deeply. They show a willingness to go to a verdict when the choice is rewarding a litigation system that feeds on hesitation. And so they perceive that the measure of a claims operation is not only how effectively it processes claims, however how nicely it delivers on the promise that each insurance coverage coverage in the end represents.

In a market formed by social inflation, nuclear verdicts, and rising expectations from business insurance coverage purchasers, these qualities aren’t desk stakes. They’re differentiators – and the 2026 5-Star Claims winners have earned the suitable to be acknowledged for them.

- AIG

- Auto-Homeowners Insurance coverage

- Chubb

- Liberty Mutual

- Nationwide

- Progressive Insurance coverage

- QBE North America

- State Farm Insurance coverage

- The Hartford

- Tokio Marine

- Vacationers

- USAA

- W. R. Berkley

{kind=link}