Mortgage charges have been rising not too long ago, however they could possibly be even worse than they’re now. As somebody who does not imagine, federal reserve has reversed course and the Federal Reserve has enacted COVID-19 housing insurance policies to stem the decline in current residence gross sales, indicating that rates of interest stay low regardless of robust inflation information and decrease charges. It is not surprising to me that it is this excessive.

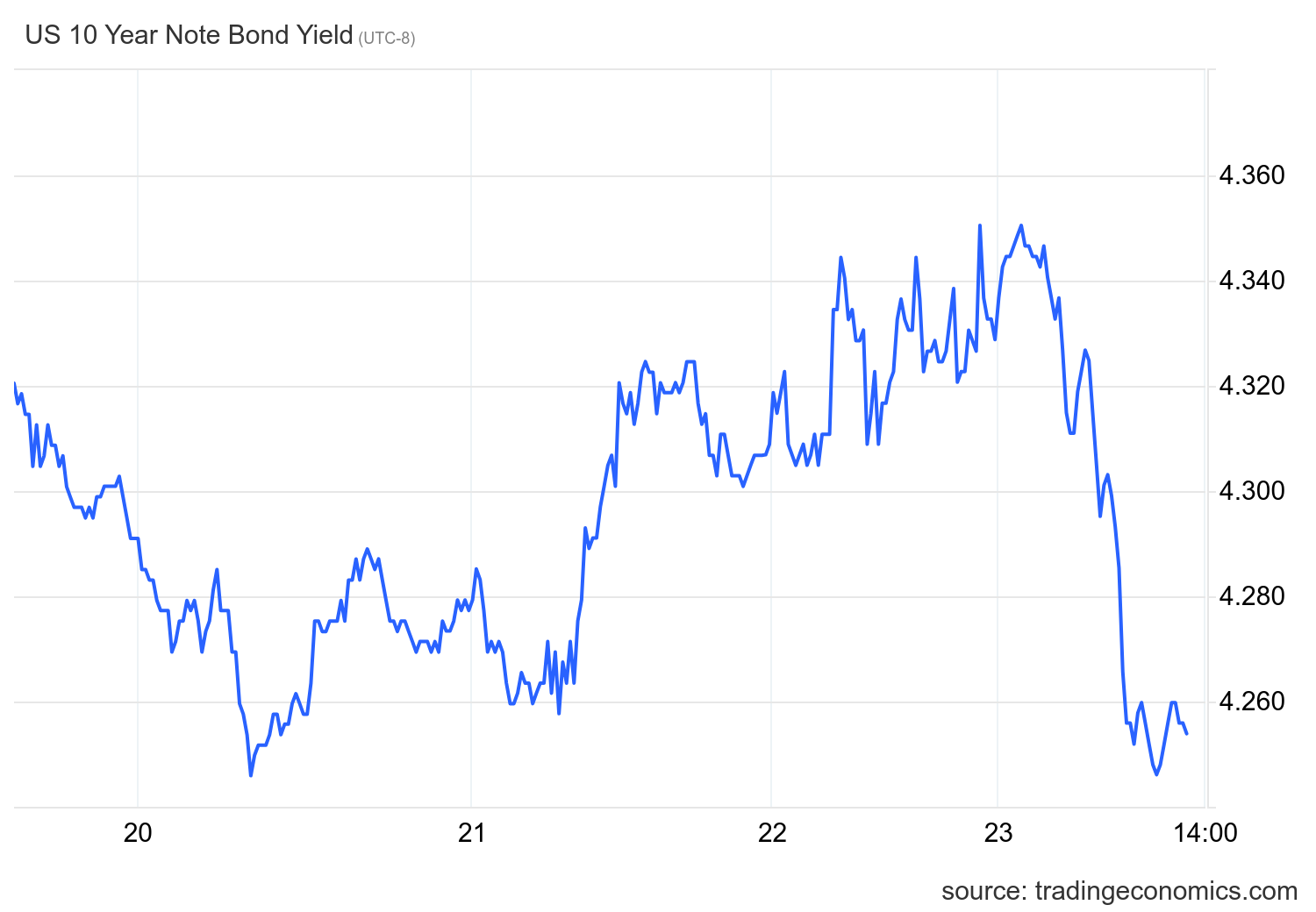

Mortgage rate of interest and 10-year yield

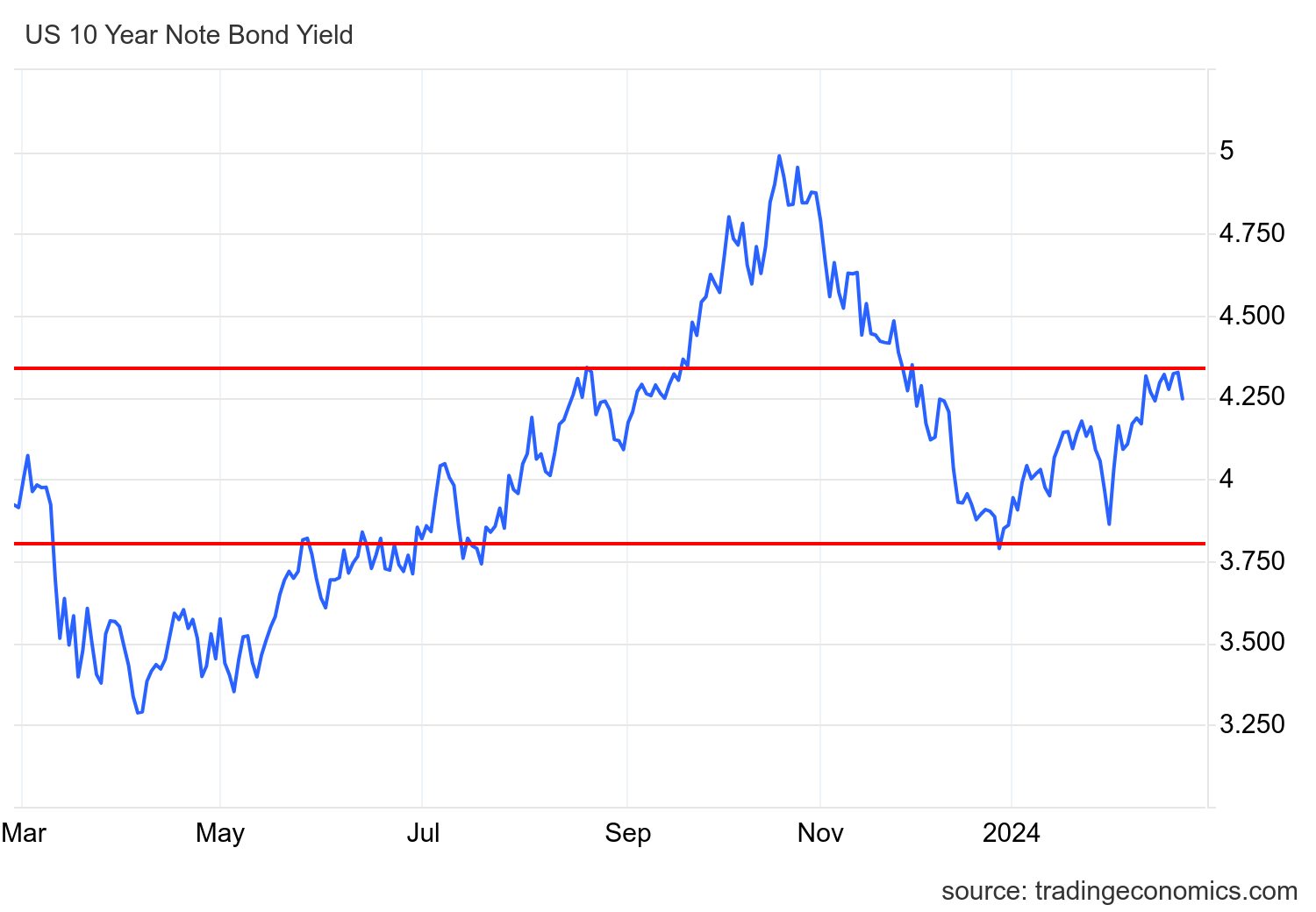

The important thing to housing in 2024 is the 10-year yield. In my 2024 prediction for him, I set the 10-year yield vary to be: 3.21%-4.25%there is a essential line within the sand 3.37%.If financial indicators are robust, it should not fall beneath this. 3.21%However that line will likely be examined if labor information weakens.

I worth labor information greater than inflation, so crucial information for me, together with mortgage charges, is unemployment claims information. With unemployment claims information enhancing not too long ago, it is no shock to me that mortgage charges and 10-year Treasury yields stay excessive.

Beneath is a take a look at the developments in 10-year bond yields over the previous few years.

Critical mortgage rate of interest story

In the event you’ve been following my woes concerning the 10-year bond yield over the previous 12 months, you may know. 4.34% Within the merry-go-round world of monitoring charges, this was an necessary stage for me. If this stage is exceeded, the Fed will likely be taking part in with fireplace once more because it did final 12 months, with the 10-year Treasury yield rising to five% once more and doubtlessly 8% mortgage charges once more. Regardless of the Fed’s many hawkish feedback final week, it has not but surpassed that stage.

A few of my 2024 predictions have been mistaken thus far this 12 months. If the 10-year Treasury yield reaches 4.25%, he predicted mortgage charges will attain 7.25%. That hasn’t occurred. The ten-year bond yield briefly exceeded this 4.25% stage, and the best residence mortgage rate of interest 7.16%. It is because spreads have improved this 12 months. If the unfold is common, your mortgage rate of interest will likely be low.

Breaking above 4.34% is an enormous deal for the 10-year bond yield. A drop beneath 3.80%, one other necessary stage for the 10-year bond yield, would even be an enormous drawback. As mentioned in a latest HousingWire Day by day podcast, reaching that can require both softer financial information or a severe change in route from the Fed. In the event you take a look at the graph beneath, you possibly can see why I assumed that bond yields wouldn’t fall a lot beneath 3.80% even after rising considerably from 5%. It will be one factor if financial indicators have been softening, however that hasn’t occurred but.

Rising inflation brought about mortgage charges to fall in late 2022 and early 2023, and the bond market anticipated both a Fed turnaround or a recession, however neither occurred, so the Fed continued to lift charges. Keep in mind, macro information and Fed expectations tremendously affect this. This is the reason I imagine in speaking about his 10-year yield channel every year reasonably than a single mortgage charge forecast.

For now, financial and labor indicators are holding up, so rates of interest stay at 7%.in this recent podcastRight here we mentioned why we do not imagine the Fed will deal with housing coverage.

Weekly housing stock information

My favourite 2024 housing information line reveals stock rising year-over-year. I imagine that housing stock may improve over time as mortgage charges rise and demand weakens. When rates of interest fall, the story of stock development disappears, so you will need to hold rates of interest excessive for a protracted time period.

Final week’s stock standing seemed like this.

- Weekly stock fluctuations (February sixteenth to February twenty third): Stock has elevated 494,029 to 497,608

- In the identical week of the earlier 12 months (February 17-24), stock was 437,282 to 430,395

- The latest inventory low was in 2022. 240,194

- The height of stock in 2023 is 569,898

- Take a look at this week’s lively checklist for context. 2015 was 958,304

New itemizing information

New itemizing information has been rising 12 months on 12 months and weekly, however we hope to see extra vital will increase. As mortgage charges rise, demand weakens and houses do not go into contract shortly. So long as individuals proceed to checklist their houses every week, this information line is prone to develop sooner.

Weekly new itemizing information for the previous few years:

- 2024: 51,381

- 2023: 44,864

- 2022: 48,979

For historic reference, from 2008 to 2011, new property information elevated by 250,000 to 400,000 new properties every week.

value discount charge

Yearly, one-third of all houses have their costs lowered earlier than they go on sale. It is a conventional housing exercise that takes place yearly. Nevertheless, this information could possibly be robust in both route if mortgage charges rise or fall sharply.

Beginning November 9, 2022, year-over-year value information is stabilizing. Even when final 12 months’s rate of interest was his 8%, the info is detrimental year-over-year and nonetheless continues to say no year-over-year. As rates of interest rise and seasonal inventories improve, extra provide enters the market and buy provide information developments detrimental, so year-over-year value discount information ought to improve in comparison with 2023 ranges. is.

Listed here are final week’s value reductions over the previous few years:

- 2024: 30.4%

- 2023: 31.1%

- 2022: 18.3%

Buy utility information

Buy request information reveals an analogous sample to final 12 months. When rates of interest rose in February, buy utility information declined.Final week, mortgage rates of interest have been 6.63% to 7.16%on the finish of the week 7.08%. This resulted in 4 consecutive weeks of detrimental information, much like final 12 months. Which means latest current residence gross sales stories that confirmed a restoration are already too outdated.

From November 2023 onwards, 8 optimistic and 4 minuses Please buy the printed utility kind after the vacation adjustment. From this 12 months to in the present day, 2 optimistic prints versus 4 detrimental prints. We’re seeing a carbon copy of what occurred in 2023. Which means even if you’re working from an all-time low gross sales stage, will probably be tough to get any actual gross sales improve. This is the reason final 12 months I talked about what the housing market was actually like. Focusing on 10-year yield.

The week forward: Housing statistics and inflation report

Quite a few housing stories will likely be launched this week, together with new residence gross sales, residence value index stories, and pending residence gross sales. Pending residence gross sales will likely be fascinating as shopping for apps are down and must be down. If not, will probably be postponed to subsequent month. In some instances, older month-to-month information might lag present forward-looking information by one to 2 months.

However the Fed’s predominant inflation measure, the PCE inflation report, will present that whereas inflation development has slowed from the height of the pandemic, it’s not but sufficient to shift coverage. As at all times, control Thursday’s unemployment claims numbers. That is crucial information line we presently have.

{kind=link}