Key takeout

- The U.S. housing finance regulators need Fannie Might and Freddie Mac to draft a plan that may deal with the crypto as a part of debtors’ property for mortgage opinions.

- Crypto-holdings will be counted immediately into mortgage underwriting if the proposal is accepted.

Please share this text

The Federal Housing and Treasury Company (FHFA) has directed mortgage giants Fanny Might and Freddie Mac to develop and submit proposals that may permit crypto property to be included in mortgage underwriting with out forcing conversion.

Order, Signed by William Pluto on June 25ththe director of FHFA got here proper after Pulte I said Housing Finance Regulators might be Monday on the lookout for the potential of together with crypto as a part of their asset valuation in mortgage eligibility.

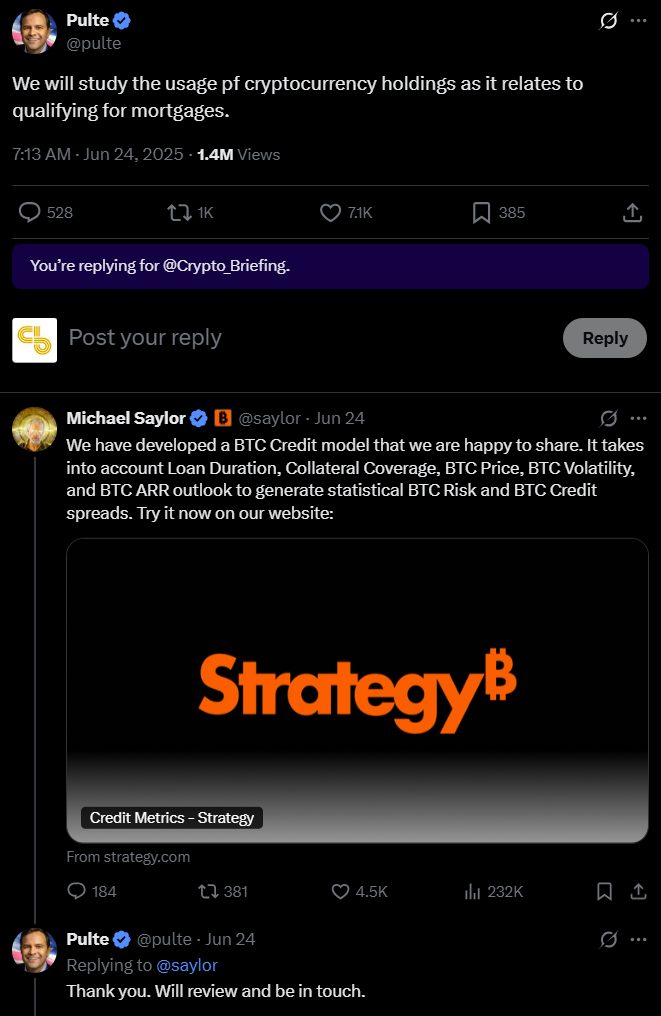

Michael Saylor, govt chairman of Technique, supplied to share the corporate’s BTC credit score mannequin. This was created to evaluate creditworthiness primarily based on the mortgage interval, collateral, Bitcoin value fluctuations, and Bitcoin property that handle threat forecasts.

In response, Pulte stated he would evaluation the mannequin of the technique.

Below the brand new order, government-sponsored firms ought to solely take into account crypto property that may be verified and held in a US regulated central change that operates inside acceptable authorized frameworks.

The order additionally requires each firms to include threat mitigation measures, corresponding to adjusting market volatility and altering acceptable risk-based adjustments to the portion of reserves held in crypto property.

The proposed adjustments have to be accepted by the board of administrators of every firm earlier than they are often submitted to FHFA for evaluation. This directive will take impact instantly and requires implementation “rationally sensible.”

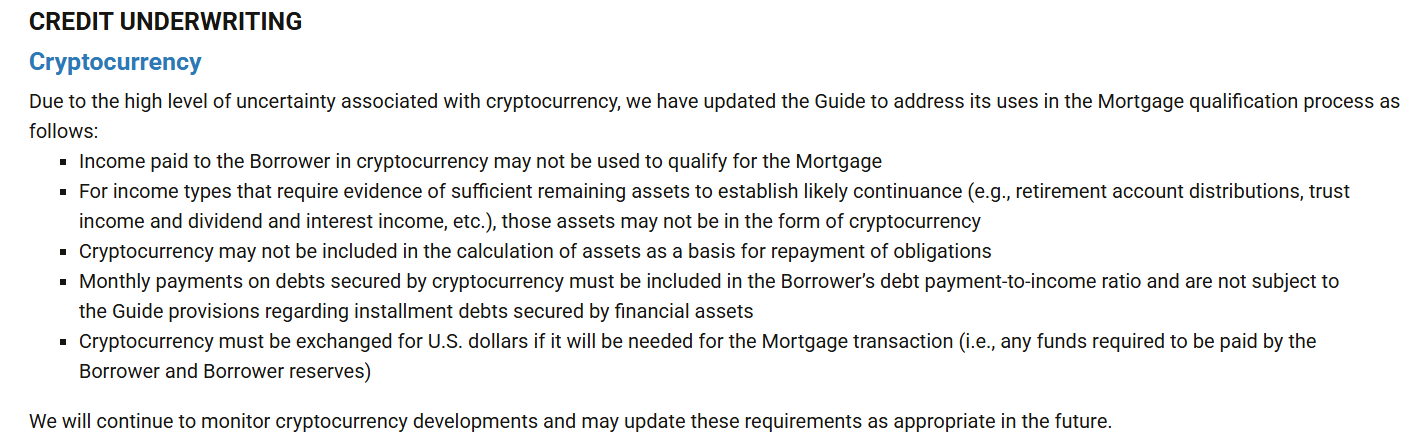

Cryptocurrencies are typically not accepted as mortgage reserves until transformed to US {dollars}. 2021 guidanceFreddie Mac explicitly acknowledged that Crypto will not be included within the calculation of property as the idea for mortgage repayments and must be exchanged for US {dollars} in mortgage transactions.

Equally, lenders are normally required to transform crypto property into money or money equivalents, counting them as reserves and counting them because of volatility and regulatory uncertainty.

If accepted, this transfer will assist cryptocurrencies absolutely combine with conventional mortgage financing and make it simpler for crypto holders to borrow.

Please share this text

{kind=link}