credit score stress knowledge

I am 100% certain that when the subsequent job-killing recession occurs, the credit score stress knowledge will go up and America’s ruined individuals shall be sitting round ineffective. YouTube and × Accounts push their unfavourable narrative continuous. However now that we now have all the info, we will see that the credit score stress knowledge we noticed through the 2008 disaster won’t ever occur once more, so long as there are qualifying mortgages in place. my crusade Over the previous decade, it has been essential to make sure that lending requirements are by no means relaxed. As a result of requirements are already liberalized right this moment, however they’re now not loopy.

The rationale I fought so onerous for this premise is that in instances of financial stress and big inflationary outbursts like we noticed within the early days of COVID-19, owners are compelled to purchase boring vanilla It’s because they’re protected by a 30-year fastened mortgage.

From the info traces beneath, we anticipated credit score stress to return to pre-COVID-19 ranges by the top of 2024, however that hasn’t occurred. Once more, everybody pushing 2008 housing must get out of there.

Use these up to date charts on credit score knowledge in your Thanksgiving dinner dialog and bear in mind why that is so essential. New itemizing knowledge we monitor Altos Research Though it has been at an all-time low for the previous few years, it was at an accelerated stage on the time. Under is an instance of knowledge for November ninth. Have a look at the distinction between this week in 2024 and the identical week from 2009 to 2011. There have been a variety of harassed sellers again then.

This week’s new itemizing knowledge:

- 2024: 48,863

- 2009: 274,614

- 2010: 359,534

- 2011: 315,915

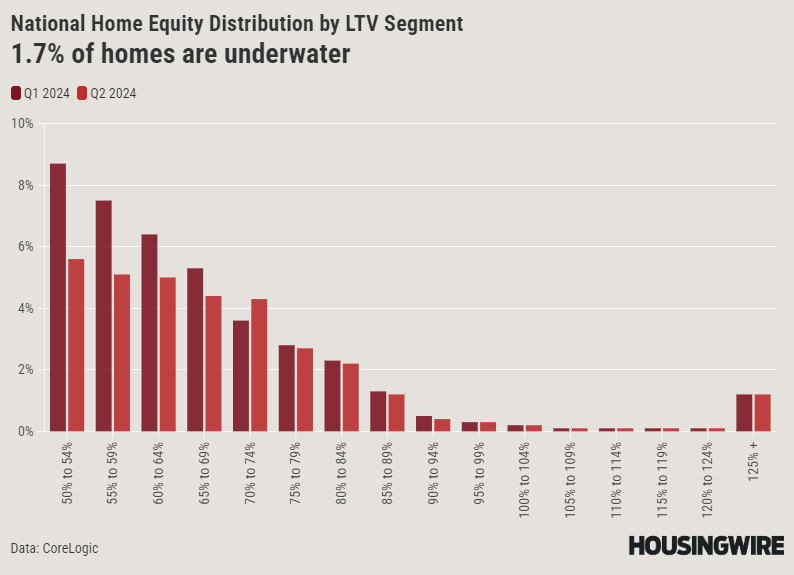

These credit-stressed sellers did not flip round and purchase one other residence, resulting in years of elevated distressed provide available on the market. Nothing like this has occurred previously decade, and it will not occur till we now have a job-killing recession. Moreover, in 2010, greater than 23% of houses had been underwater. Right now, it’s the lowest share ever.

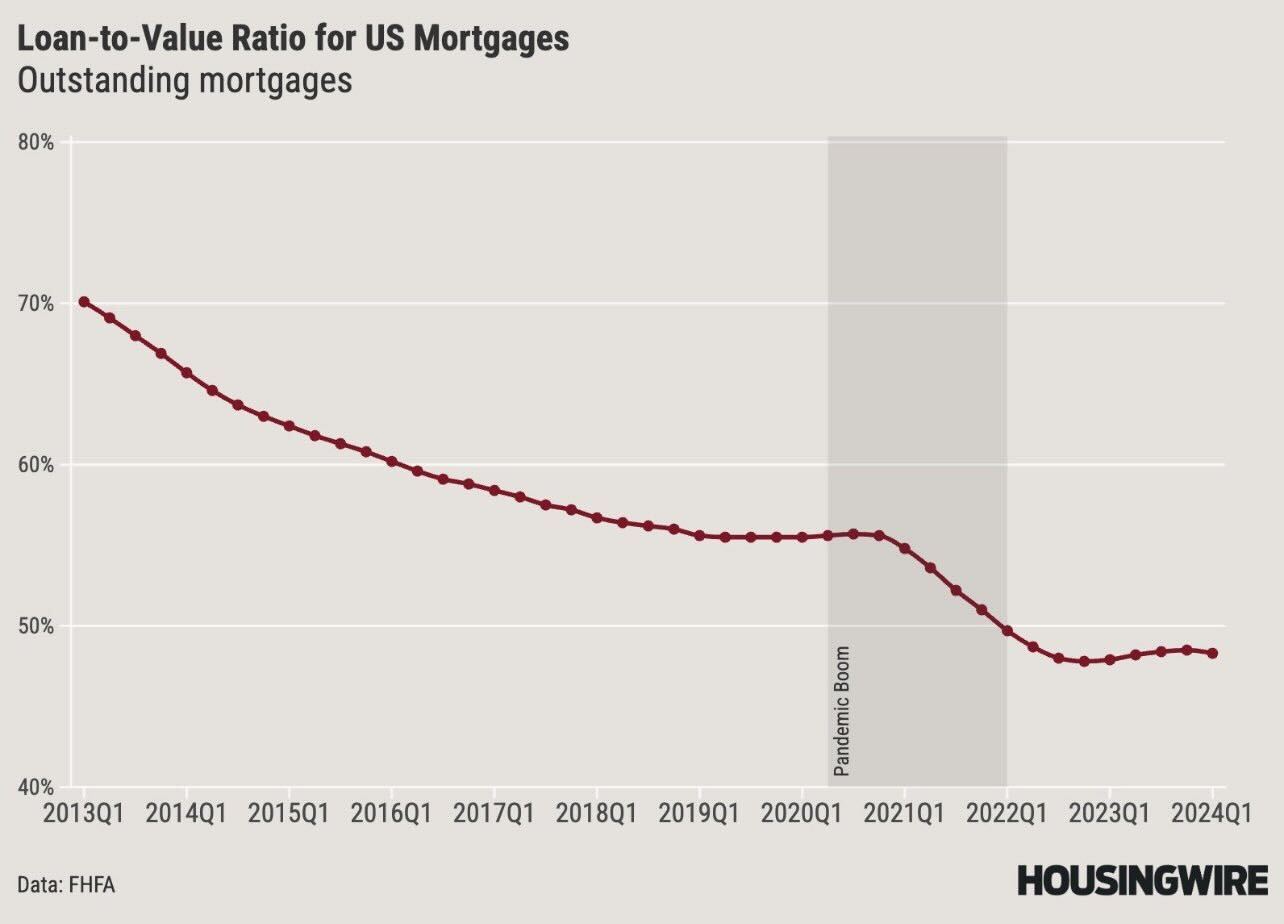

There are different issues to think about. Presently, greater than 40% of houses do not also have a mortgage, and people who do have a loan-to-value ratio of lower than 50% on common. In 2008, loan-to-value was almost 85%. Moreover, this 12 months’s median down fee knowledge is 15%, that means owners have extra freedom than they did again then.

I hope all of those graphs clear up some confusion for Uncle Dave and different Thanksgiving friends questioning if we’ll see one other housing crash just like the one in 2008. House owner credit score knowledge tells a special story.

{kind=link}