House costs have remained regular over the previous two months regardless of rising mortgage charges and stock information. Our weekly tracker information is created to look past conventional month-to-month experiences like Case-Shiller and NAR’s Current House Gross sales Report, however what I’ve seen over the previous few weeks has shocked me. Ta.

I wish to present you the way the information has modified as mortgage charges transfer in the direction of 6%. That method, the subsequent time this occurs, you will have a greater concept of what to anticipate within the housing market.

Knowledge deviation

My goal is to find out the extent of mortgage rates of interest required to vary the demand curve. This will likely additionally change the worth curve of housing information. I’ve lengthy thought it uncommon that since 1996, the variety of current residence gross sales in the US has trended under 4 million. There have been a number of months under this stage, however nothing too dramatic.

Again on November 9, 2022, I confirmed how monitoring forward-looking information may change housing tendencies. this podcast video is a tutorial on tips on how to observe this and why folks acquired the 2023 home value crash unsuitable as a result of they did not have a working mannequin. To this present day, these rules nonetheless apply. Let’s check out what’s modified between now and the previous two years.

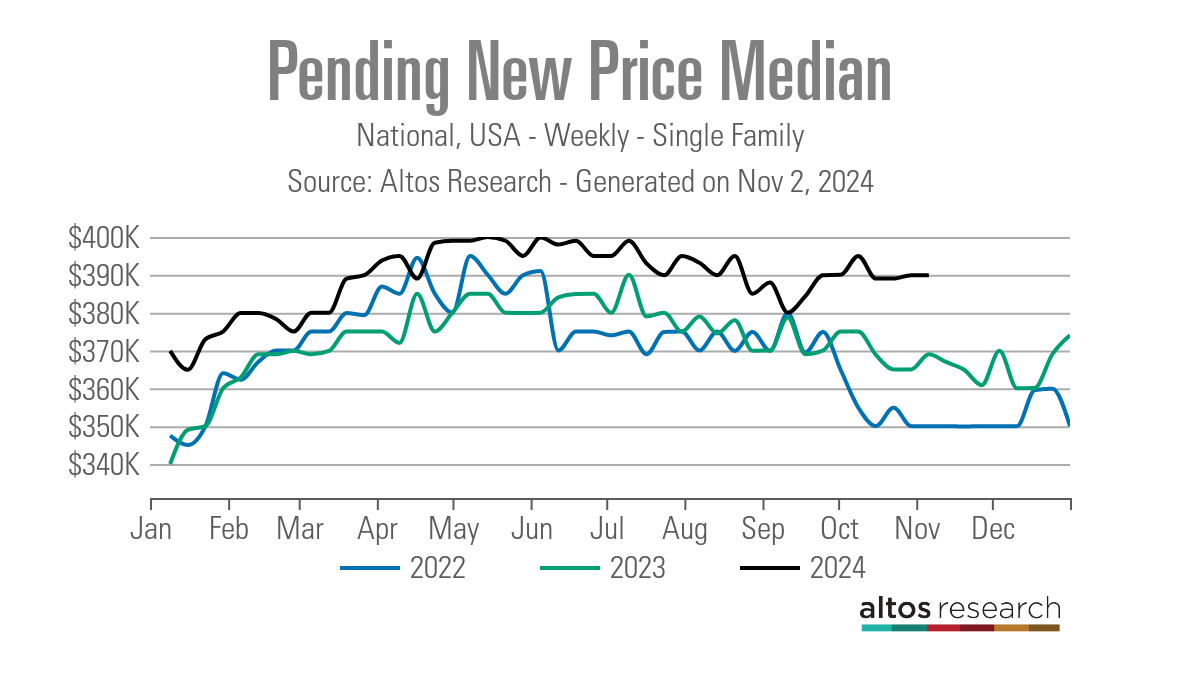

pending contract

First, we should acknowledge that whenever you translate these numbers into labor pressure, that is the third calendar yr by which residence gross sales are at an all-time low. It isn’t like your mortgage is underwater or your credit score is tight. That is the most important collapse in historical past, and gross sales stay low.

It’s because mortgage rates of interest have remained between 6% and eight% for the previous two years as costs have risen, and gross sales under this stage is not going to plummet, so the gross sales hurdle for our firm is low. means. So in case you have a look at the contract information, you may see that the information is stable with mortgage charges coming down in the direction of 6%, however the information continues to be off the 2022 and 2023 ranges. Which means that bottom-end gross sales are steady. A base for work.

The conclusion I draw from that is that we’d like a 6% mortgage price to develop gross sales with a point of sustainability. It isn’t nice, however it’s potential to develop at that stage and preserve increased gross sales charges. You need not get your mortgage price to three%, 4%, and even 5%, however simply aiming for six% and staying there can assist.

If you wish to see stable gross sales progress, you want a mortgage price and time period under 6%, however we will not even predict that stage but, so till the labor market collapses or spreads get higher, we’re in all probability headed in that route. I do not plan on going. Significantly better. we talked about this not too long ago above CNBC. That is one thing to contemplate sooner or later. Annually, as wages rise, extra households kind, and mortgage charges fall, a brand new constructive demand curve information line over 12 weeks must be created. Nonetheless, if mortgage charges could be maintained between 5.75% and 6.25% for 12 months, increased gross sales ranges may very well be sustained from confirmed information from the tip of 2022 onwards.

Buy utility information

Final week’s buy request information was up 5% in comparison with the earlier week and 10% in comparison with the earlier yr. However let’s not neglect that October’s bar was shallow. So take your complete month of constructive year-over-year progress and provides it some context. In the event you take your complete month of October, which was constructive each week on a year-over-year foundation, the common year-over-year progress price was about 7.4%.

Let’s check out how this information line has behaved up to now this yr.

When mortgage charges have been rising earlier this yr (6.75% to 7.50%), buy utility information seemed like this:

- 14 damaging prints

- 2 flat prints

- 2 constructive prints

Since mortgage charges began falling in mid-June, buy affords have been:

- 12 constructive prints

- 5 damaging prints

- 1 flat print

- Recorded constructive progress yr on yr for 3 consecutive years

With mortgage charges rising once more, we discover ourselves within the following state of affairs.

- 2 damaging prints

- 1 constructive print each week

We see a transparent and constructive information line right here with mortgage charges heading in the direction of 6%. This has resulted in two situations since late 2022 the place demand improved for greater than 12 weeks. I discussed that the latest information is completely different. Housing Wire Daily Podcast final week. However not solely demand is essential, but in addition value.

value information

In the case of value discount information, many pretend housing specialists acquired their info from different sources and did not know tips on how to clarify it correctly. By the best way, this is without doubt one of the funniest issues to look at in 2024. They misinterpreted the rise in low cost charges and stock information to imply that residence costs throughout the nation needed to fall considerably this yr. Nonetheless, we have now by no means had a correct deep damaging value curve information line this yr, and it’s now November.

Nonetheless, with mortgage charges heading in the direction of 6% this yr, it was potential that low cost price information from the start of this yr can be decrease than information for 2022 and 2023. Nothing too dramatic right here, however as you may see with the pending contact information, there’s a price variable that may change the information line at the same time as housing stock will increase.

We’ve years of housing information from the early-to-mid Nineteen Eighties, mid-to-late Nineties, and even 2000 to 2005 that present stock progress. and sale. Inventories might improve, gross sales might improve, and costs might rise. Markdown information is essential if you understand how to learn it appropriately. As you may see under, markdown information has slowed not too long ago.

What’s stunning is that the brand new weekly median pending value information stays strong even during times of seasonal value weak point, particularly now as stock information will increase. There’s a clear discrepancy between the 2022 and 2023 information, as proven under. That is why my forecast for 2024 is 2.33%, placing home value progress in danger. It does not take a rocket scientist to guess what the information line is telling us if mortgage charges keep round 6%.

Weekly information row

I am specializing in tracker deviation information this weekend. That is completely different from what we usually do. It is a abstract of the normal information we offered.

Weekly housing stock decreased barely. Inventories continued to say no barely this week. For individuals who thought it was inconceivable for stock to develop any sooner this yr because of the vital improve in energetic itemizing information, we hope 2024 adjustments your thoughts.

stock has fallen 736,014 to 735,718.

This week’s new itemizing information is 60,066 to 60,819.

The brilliant spot for 2024 up to now is that inventories are rising. We had hoped to realize this in 2023, however it was too late to make any vital adjustments. Nonetheless, for 2024, we see a rise in stock, and new itemizing information for 2024 doesn’t present any new harsh itemizing information. To get some perspective on what a annoying preliminary public providing is like, evaluate: 60,819 Comparability of this week’s new listings information with information from these years seen this week:

- 2009: 280,400

- 2010: 353,457

- 2011: 352,030

As I typically say, there was a special credit score market again then, so cease dancing with ghosts.

10 yr yield and mortgage rate of interest

My predictions for 2024 included:

- Mortgage rates of interest vary from 7.25% to five.75%.

- The ten-year yield vary is 4.25% to three.21%.

I am going to attempt to preserve it so simple as potential. I have been speaking about this 4.40% line on the 10-year bond yield. Breaking above this stage would break the downward pattern in 10-year Treasury yields that started at 5% on October 16, 2023. There’s so much occurring this week, so keep tuned. In the event you’re confused in regards to the bond market motion on Jobs Friday, this text will clarify my tackle it.

mortgage unfold

Mortgage spreads have been sturdy on Friday, avoiding a deterioration in costs. However the greater story is that this yr’s enchancment in spreads has been constructive for housing. If there isn’t a enchancment this yr, rates of interest may very well be increased not solely right this moment however all year long. Spreads have worsened not too long ago, however are nonetheless higher than final yr.

Subsequent week: All bets are off

Between the election and this week’s Fed assembly, all bets are off as as to whether there will likely be normalcy. I will be on the HousingWire Each day podcast thrice this week to clarify what is going on on. On Monday’s podcast, we attempt to clarify what is going on on with the 10-year Treasury yield and mortgage charges.

Bond yields on the 4.40% stage will likely be key this week. Exiting above that stage and receiving follow-through bond gross sales may very well be problematic for housing. Nonetheless, attempt to ignore any motion through the day. When the expertise stage approaches a essential stage, it could fluctuate wildly. Everybody, please do your greatest this week.

{kind=link}