Intelligently synergizing dynamic programming and Monte Carlo algorithms

Reinforcement studying is a site in machine studying that introduces the idea of an agent studying optimum methods in complicated environments. The agent learns from its actions, which end in rewards, based mostly on the surroundings’s state. Reinforcement studying is a difficult subject and differs considerably from different areas of machine studying.

What’s outstanding about reinforcement studying is that the identical algorithms can be utilized to allow the agent adapt to fully totally different, unknown, and sophisticated situations.

Notice. To completely perceive the ideas included on this article, it’s extremely really useful to be acquainted with dynamic programming and Monte Carlo methods mentioned in earlier articles.

- In part 2, we explored the dynamic programming (DP) method, the place the agent iteratively updates V- / Q-functions and its coverage based mostly on earlier calculations, changing them with new estimates.

- In parts 3 and 4, we launched Monte Carlo (MC) strategies, the place the agent learns from expertise acquired by sampling episodes.

Temporal-difference (TD) studying algorithms, on which we’ll focus on this article, mix rules from each of those apporaches:

- Just like DP, TD algorithms replace estimates based mostly on the data of earlier estimates. As seen partially 2, state updates might be carried out with out up to date values of different states, a method often called bootstrapping, which is a key function of DP.

- Just like MC, TD algorithms don’t require data of the surroundings’s dynamics as a result of they be taught from expertise as nicely.

This text is predicated on Chapter 6 of the guide “Reinforcement Learning” written by Richard S. Sutton and Andrew G. Barto. I extremely admire the efforts of the authors who contributed to the publication of this guide.

As we already know, Monte Carlo algorithms be taught from expertise by producing an episode and observing rewards for each visited state. State updates are carried out solely after the episode ends.

Temporal-difference algorithms function equally, with the one key distinction being that they don’t wait till the tip of episodes to replace states. As a substitute, the updates of each state are carried out after n time steps the state was visited (n is the algorithm’s parameter). Throughout these noticed n time steps, the algorithm calculates the obtained reward and makes use of that data to replace the beforehand visited state.

Temporal-difference algorithm performing state updates after n time steps is denoted as TD(n).

The only model of TD performs updates within the subsequent time step (n = 1), often called one-step TD.

On the finish of the previous part, we launched the constant-α MC algorithm. It seems that the pseudocode for one-step TD is nearly similar, apart from the state replace, as proven beneath:

Since TD strategies don’t wait till the tip of the episode and make updates utilizing present estimates, they’re mentioned to make use of bootstrapping, like DP algorithms.

The expression within the brackets within the replace formulation is named TD error:

On this equation, γ is the low cost issue which takes values between 0 and 1 and defines the significance weight of the present reward in comparison with future rewards.

TD error performs an vital function. As we’ll see later, TD algorithms might be tailored based mostly on the type of TD error.

At first sight, it might sound unclear how utilizing data solely from the present transition reward and the state values of the present and subsequent states might be certainly helpful for optimum technique search. Will probably be simpler to know if we check out an instance.

Allow us to think about a simplified model of the well-known “Copa America” soccer match, which often takes place in South America. In our model, in each Copa America match, our group faces 6 opponents in the identical order. Via the system just isn’t actual, we’ll omit complicated particulars to raised perceive the instance.

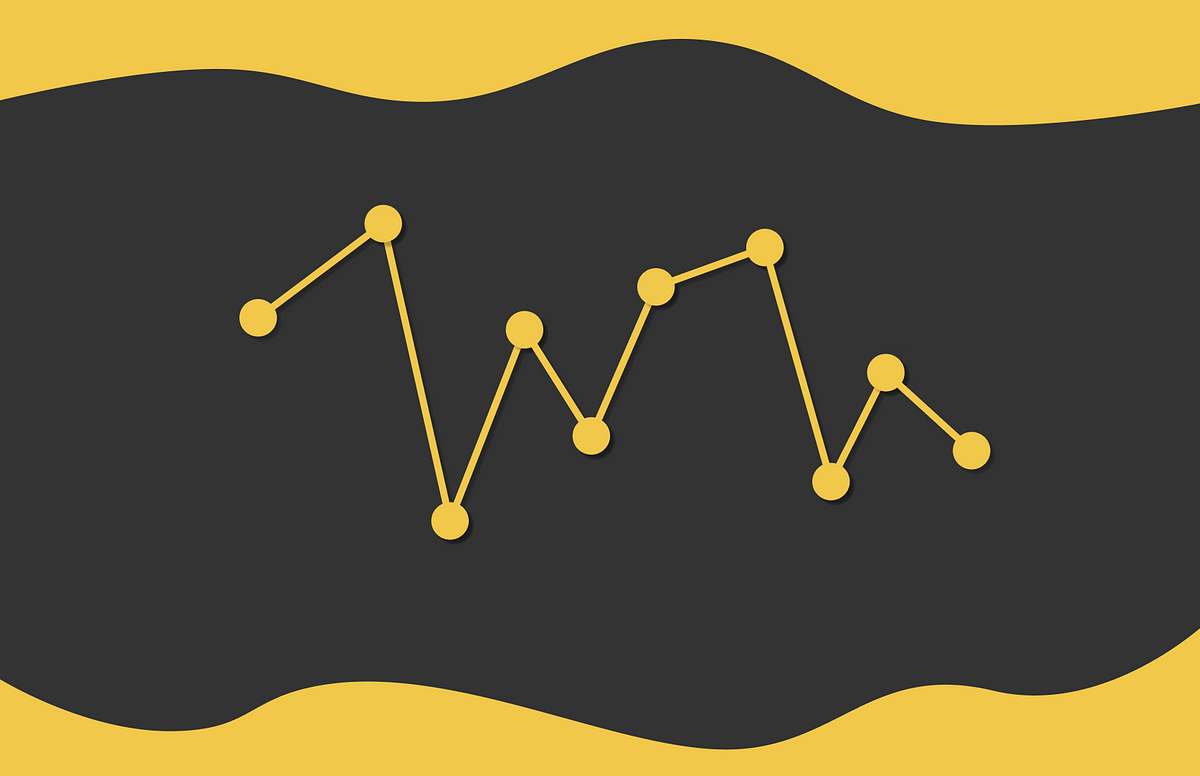

We want to create an algorithm that can predict our group’s whole aim distinction after a sequence of matches. The desk beneath reveals the group’s outcomes obtained in a latest version of the Copa America.

To higher dive into the information, allow us to visualize the outcomes. The preliminary algorithm estimates are proven by the yellow line within the diagram beneath. The obtained cumulative aim distinction (final desk column) is depicted in black.

Roughly talking, our goal is to replace the yellow line in a method that can higher adapt modifications, based mostly on the latest match outcomes. For that, we’ll examine how constant-α Monte Carlo and one-step TD algorithms deal with this job.

Fixed-α Monte Carlo

The Monte Carlo technique calculates the cumulative reward G of the episode, which is in our case is the whole aim distinction in any case matches (+3). Then, each state is up to date proportionally to the distinction between the whole episode’s reward and the present state’s worth.

As an illustration, allow us to take the state after the third match towards Peru (we’ll use the training price α = 0.5)

- The preliminary state’s worth is v = 1.2 (yellow level equivalent to Chile).

- The cumulative reward is G = 3 (black dashed line).

- The distinction between the 2 values G–v = 1.8 is then multiplied by α = 0.5 which supplies the replace step equal to Δ = 0.9 (purple arrow equivalent to Chile).

- The brand new worth’s state turns into equal to v = v + Δ = 1.2 + 0.9 = 2.1 (purple level equivalent to Chile).

One-step TD

For the instance demonstration, we’ll take the whole aim distinction after the fourth match towards Chile.

- The preliminary state’s worth is v[t] = 1.5 (yellow level equivalent to Chile).

- The following state’s worth is v[t+1]= 2.1 (yellow level equivalent to Ecuador).

- The distinction between consecutive state values is v[t+1]–v[t] = 0.6 (yellow arrow equivalent to Chile).

- Since our group received towards Ecuador 5 : 0, then the transition reward from state t to t + 1 is R = 5 (black arrow equivalent to Ecuador).

- The TD error measures how a lot the obtained reward is larger compared to the state values’ distinction. In our case, TD error = R –(v[t+1]–v[t]) = 5–0.6 = 4.4 (purple clear arrow equivalent to Chile).

- The TD error is multiplied by the training price a = 0.5 which results in the replace step β = 2.2 (purple arrow equivalent to Chile).

- The brand new state’s worth is v[t] = v[t] + β = 1.5 + 2.2 = 3.7 (purple level equivalent to Chile).

Comparability

Convergence

We are able to clearly see that the Monte Carlo algorithm pushes the preliminary estimates in direction of the episode’s return. On the identical time, one-step TD makes use of bootstrapping and updates each estimate with respect to the subsequent state’s worth and its speedy reward which usually makes it faster to adapt to any modifications.

As an illustration, allow us to take the state after the primary match. We all know that within the second match our group misplaced to Argentina 0 : 3. Nevertheless, each algorithms react completely otherwise to this situation:

- Regardless of the unfavourable outcome, Monte Carlo solely considers the general aim distinction in any case matches and pushes the present state’s worth up which isn’t logical.

- One-step TD, then again, takes into consideration the obtained outcome and instanly updates the state’s worth down.

This instance demonstrates that in the long run, one-step TD performs extra adaptive updates, resulting in the higher convergence price than Monte Carlo.

The idea ensures convergence to the right worth perform in TD strategies.

Replace

- Monte Carlo requires the episode to be ended to in the end make state updates.

- One step-TD permits updating the state instantly after receiving the motion’s reward.

In lots of circumstances, this replace facet is a big benefit of TD strategies as a result of, in follow, episodes might be very lengthy. In that case, in Monte Carlo strategies, the whole studying course of is delayed till the tip of an episode. That’s the reason TD algorithms be taught sooner.

After overlaying the fundamentals of TD studying, we are able to now transfer on to concrete algorithm implementations. Within the following sections we’ll give attention to the three hottest TD variations:

- Sarsa

- Q-learning

- Anticipated Sarsa

As we realized within the introduction to Monte Carlo strategies in part 3, to seek out an optimum technique, we have to estimate the state-action perform Q slightly than the worth perform V. To perform this successfully, we regulate the issue formulation by treating state-action pairs as states themselves. Sarsa is an algorithm that opeates on this precept.

To carry out state updates, Sarsa makes use of the identical formulation as for one-step TD outlined above, however this time it replaces the variable with the Q-function values:

The Sarsa title is derived by its replace rule which makes use of 5 variables within the order: (S[t], A[t], R[t + 1], S[t + 1], A[t + 1]).

Sarsa management operates equally to Monte Carlo management, updating the present coverage greedily with respect to the Q-function utilizing ε-soft or ε-greedy insurance policies.

Sarsa in an on-policy technique as a result of it updates Q-values based mostly on the present coverage adopted by the agent.

Q-learning is likely one of the hottest algorithms in reinforcement studying. It’s nearly similar to Sarsa apart from the small change within the replace rule:

The one distinction is that we changed the subsequent Q-value by the utmost Q-value of the subsequent state based mostly on the optimum motion that results in that state. In follow, this substitution makes Q-learning is extra performant than Sarsa in most issues.

On the identical time, if we rigorously observe the formulation, we are able to discover that the whole expression is derived from the Bellman optimality equation. From this angle, the Bellman equation ensures that the iterative updates of Q-values result in their convergence to optimum Q-values.

Q-learning is an off-policy algorithm: it updates Q-values based mostly on the very best determination that may be taken with out contemplating the behaviour coverage utilized by the agent.

Anticipated Sarsa is an algorithm derived from Q-learning. As a substitute of utilizing the utmost Q-value, it calculates the anticipated Q-value of the subsequent action-state worth based mostly on the chances of taking every motion beneath the present coverage.

In comparison with regular Sarsa, Anticipated Sarsa requires extra computations however in return, it takes into consideration extra data at each replace step. In consequence, Anticipated Sarsa mitigates the influence of transition randomness when choosing the subsequent motion, notably in the course of the preliminary phases of studying. Due to this fact, Anticipated Sarsa provides the benefit of larger stability throughout a broader vary of studying step-sizes α than regular Sarsa.

Anticipated Sarsa is an on-policy technique however might be tailored to an off-policy variant just by using separate behaviour and goal insurance policies for knowledge era and studying respectively.

Up till this text, we’ve got been discussing a set algorithms, all of which make the most of the maximization operator throughout grasping coverage updates. Nevertheless, in follow, the max operator over all values results in overestimation of values. This problem notably arises in the beginning of the training course of when Q-values are initialized randomly. Consequently, calculating the utmost over these preliminary noisy values usually leads to an upward bias.

As an illustration, think about a state S the place true Q-values for each motion are equal to Q(S, a) = 0. Resulting from random initialization, some preliminary estimations will fall beneath zero and one other half can be above 0.

- The utmost of true values is 0.

- The utmost of random estimates is a optimistic worth (which is named maximization bias).

Instance

Allow us to contemplate an instance from the Sutton and Barto guide the place maximization bias turns into an issue. We’re coping with the surroundings proven within the diagram beneath the place C is the preliminary state, A and D are terminal states.

The transition reward from C to both B or D is 0. Nevertheless, transitioning from B to A leads to a reward sampled from a standard distribution with a imply of -0.1 and variance of 1. In different phrases, this reward is unfavourable on common however can sometimes be optimistic.

Principally, on this surroundings the agent faces a binary selection: whether or not to maneuver left or proper from C. The anticipated return is obvious in each circumstances: the left trajectory leads to an anticipated return G = -0.1, whereas the proper path yields G = 0. Clearly, the optimum technique consists of at all times going to the proper aspect.

Alternatively, if we fail to handle the maximization bias, then the agent could be very more likely to prioritize the left path in the course of the studying course of. Why? The utmost calculated from the conventional distribution will end in optimistic updates to the Q-values in state B. In consequence, when the agent begins from C, it would greedily select to maneuver to B slightly than to D, whose Q-value stays at 0.

To achieve a deeper understanding of why this occurs, allow us to carry out a number of calculations utilizing the folowing parameters:

- studying price α = 0.1

- low cost price γ = 0.9

- all preliminary Q-values are set to 0.

Iteration 1

Within the first iteration, the Q-value for going to B and D are each equal to 0. Allow us to break the tie by arbitrarily selecting B. Then, the Q-value for the state (C, ←) is up to date. For simplicity, allow us to assume that the utmost worth from the outlined distribution is a finite worth of three. In actuality, this worth is larger than 99% percentile of our distribution:

The agent then strikes to A with the sampled reward R = -0.3.

Iteration 2

The agent reaches the terminal state A and a brand new episode begins. Ranging from C, the agent faces the selection of whether or not to go to B or D. In our situations, with an ε-greedy technique, the agent will nearly choose going to B:

The analogous replace is then carried out on the state (C, ←). Consequently, its Q-value will get solely larger:

Regardless of sampling a unfavourable reward R = -0.4 and updating B additional down, it doesn’t alter the scenario as a result of the utmost at all times stays at 3.

The second iteration terminates and it has solely made the left path extra prioritized for the agent over the proper one. In consequence, the agent will proceed making its preliminary strikes from C to the left, believing it to be the optimum selection, when the truth is, it’s not.

One essentially the most elegant options to remove maximization bias consists of utilizing the double studying algorithm, which symmetrically makes use of two Q-function estimates.

Suppose we have to decide the maximizing motion and its corresponding Q-value to carry out an replace. The double studying method operates as follows:

- Use the primary perform Q₁ to seek out the maximizing motion a⁎ = argmaxₐQ₁(a).

- Use the second perform Q₂ to estimate the worth of the chosen motion a⁎.

The each features Q₁ and Q₂ can be utilized in reverse order as nicely.

In double studying, just one estimate Q (not each) is up to date on each iteration.

Whereas the primary Q-function selects the most effective motion, the second Q-function supplies its unbiased estimation.

Instance

We can be wanting on the instance of how double studying is utilized to Q-learning.

Iteration 1

For example how double studying operates, allow us to contemplate a maze the place the agent can transfer one step in any of 4 instructions throughout every iteration. Our goal is to replace the Q-function utilizing the double Q-learning algorithm. We are going to use the training price α = 0.1 and the low cost price γ = 0.9.

For the primary iteration, the agent begins at cell S = A2 and, following the present coverage, strikes one step proper to S’ = B2 with the reward of R = 2.

We assume that we’ve got to make use of the second replace equation within the pseudocode proven above. Allow us to rewrite it:

Since our agent strikes to state S’ = B2, we have to use its Q-values. Allow us to have a look at the present Q-table of state-action pairs together with B2:

We have to discover an motion for S’ = B2 that maximizes Q₁ and in the end use the respective Q₂-value for a similar motion.

- The utmost Q₁-value is achieved by taking the ← motion (q = 1.2, purple circle).

- The corresponding Q₂-value for the motion ← is q = 0.7 (yellow circle).

Allow us to rewrite the replace equation in an easier kind:

Assuming that the preliminary estimate Q₂(A2, →) = 0.5, we are able to insert values and carry out the replace:

Iteration 2

The agent is now positioned at B2 and has to decide on the subsequent motion. Since we’re coping with two Q-functions, we’ve got to seek out their sum:

Relying on a kind of our coverage, we’ve got to pattern the subsequent motion from a distribution. As an illustration, if we use an ε-greedy coverage with ε = 0.08, then the motion distribution could have the next kind:

We are going to suppose that, with the 94% likelihood, we’ve got sampled the ↑ motion. Which means the agent will transfer subsequent to the S’ = B3 cell. The reward it receives is R = -3.

For this iteration, we assume that we’ve got sampled the primary replace equation for the Q-function. Allow us to break it down:

We have to know Q-values for all actions equivalent to B3. Right here they’re:

Since this time we use the primary replace equation, we take the utmost Q₂-value (purple circle) and use the respective Q₁-value (yellow circle). Then we are able to rewrite the equation in a simplified kind:

After making all worth substitutions, we are able to calculate the ultimate outcome:

We have now regarded on the instance of double Q-learning, which mitigates the maximization bias within the Q-learning algorithm. This double studying method can be prolonged as nicely to Sarsa and Anticipated Sarsa algorithms.

As a substitute of selecting which replace equation to make use of with the p = 0.5 likelihood on every iteration, double studying might be tailored to iteratively alternate between each equations.

Regardless of their simplicity, temporal distinction strategies are amongst essentially the most extensively used methods in reinforcement studying right now. What can also be attention-grabbing is which can be additionally extensively utilized in different prediction issues comparable to time sequence evaluation, inventory prediction, or climate forecasting.

To date, we’ve got been discussing solely a particular case of TD studying when n = 1. As we’ll see within the subsequent article, it may be helpful to set n to increased values in sure conditions.

We have now not lined it but, however it seems that management for TD algorithms might be carried out by way of actor-critic strategies which can be mentioned on this sequence sooner or later. For now, we’ve got solely reused the concept of GPI launched in dynamic programming algorithms.

All photos until in any other case famous are by the writer.

{kind=link}